The real action was in the volatility products (VXX, UVXY) as the VIX shot up almost doubling to the low 20s which last happened in January when the SPX had dropped to the low 1900s. The result has pushed the intermediate Indicator Scoreboard to two-thirds the levels of the July 2015 decline in the SPX from 2135 to 2044.

The strong influence of the volatility instruments is seen by the VXX $ Volume where levels have reached the levels of the July 2015 selloff.

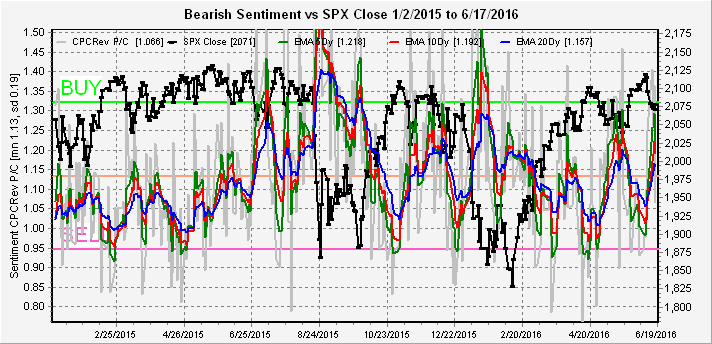

While other broader measures, such the CPC Revised (less VIX puts and calls) have shown only a moderate response to the current decline.

Conclusion. There is a disconnect between prices and volatility which is likely to be closed. Intermediate term it is likely that we see at least SPX 2120 again due to high bearish levels, but it is very possible given the BREXIT vote next week that the SPX drops to the low 2000s before a strong rally,

Weekly trade alert. Last week's short was closed for a gain of 38 SPX points out of a possible 70. For this week, flipping a coin is not a valid investment strategy, so not position before the BREXIT vote. Going long after a bottom is put in or shorting after a top is a much less risky trade. Updates if needed @mrktsignals.

No comments:

Post a Comment