Last week started much as expected with the SPX rising toward the 4450 area

by Wed (4443 act)., and following the M/W/F options OI targets. Oddly,

Tu/Th were both negative with Thur particularly violent following the NVDA EPS

outlook which took the after hours SPX (FX) to 4474 which meet the minimum

target of a 50%+ retrace (4471) of the Aug decline (4607-4335). EW

analysts almost unanimously started clamoring for 5 waves down to SPX 4250 to

confirm a larger move down, but Fri late recovery to SPX 4406, from a Powell's

hawkish speech at Jackson Hole and selloff to the SPX 4350s, may have voided that

outlook. Bonds remain a major concern as Mon saw the TNX spike to 4.36% to

take out the Oct 2022 high of 4.33% before reversing to 4.2%. The possible

"handle" of the TNX cup and handle remains questionable with bond sentiment

(TBT/TLT) remaining near the strong Sell.

Bearish sentiment increased slightly overall even as price rose overall with

a strong Buy remaining ST for the Hedge Spread indicator. COT data shows a

strong increase in bearish sentiment for the DJIA (YM) rising from a neutral

level to +.75 SD, just short of a weak Buy. Last week I indicated that for

one scenario to the SPX 4550+ area, I expected an expanding wedge in price and

time, so to clarify, a 2-3 week decline early Aug (a) would lead to a 4-6 week

rally into mid-late Sept (b) then a 8-12 week decline Oct-Dec (c).

The SPX option components for the INT/LT Composite indicator have been

removed this week due to previous problems with the volume of 0DTE options.

I. Sentiment Indicators

The INT/LT Composite indicator (outlook 3 to 6+ months) has three separate

components. Starting Aug 26, 2023 SPX options are removed due to extreme 0DTE volume

distortions. New weights are ETF put-call indicator (30%), SPX 2X ETF INT

ratio (40%), and a volatility indicator (30%) which combines the options

volatility spread of the ST SPX (VIX) to the ST VIX (VVIX) (20%) with the UVXY $ volume (10%).

Update Alt. Bearish sentiment since the beginning of Aug has risen from a

weak Sell to above neutral.

Update Alt EMA. Bearish sentiment looks a lot like Jan-Feb 2021 where a minor

correction unfolded, but prices continued to rise for about a year.

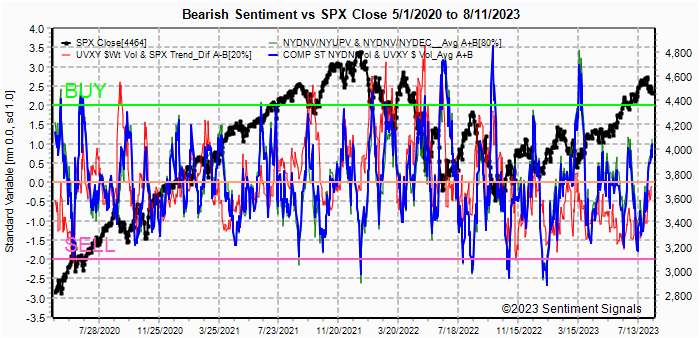

The ST Composite as a ST (1-4 week) indicator includes the NYSE volume ratio

indicator (NYDNV/NYUPV & NYDNV/NYDEC) and the UVXY $ Vol/SPX Trend. Weights

are 80%/20%.

Update. Bearish sentiment rose modestly Thur-Fri with the increased

volatility.

Update EMA. Bearish sentiment rose last week, but remains below the weak Buy.

This may be following the path after May 2021 where prices rose slowly until

sentiment picked up.

The ST/INT Composite indicator (outlook 1 to 3 months) is based on the Hedge Spread (48%)

and includes ST Composite (12%) and three options FOMO indicators using SPX (12%),

ETF (12%), and Equity (12%) calls compared to the NY ADV/DEC issues (inverted). FOMO

is shown when strong call volume is combined with strong NY ADV/DEC. See

Investment Diary

addition for full discussion.

Update EMA. Bearish sentiment remains around the neutral level.

Bonds (TNX). Bearish sentiment remains in the weak Sell area

which continues to surprise. In 2017-18 rates rose from 1.3% to 3.3% and

bearishness was extremely strong before the 2019-2020 rate decline, but now

after a 4% rise from .5%, everyone is bullish.

For the INT outlook with LT still negative, the gold miners (HUI) bearish

sentiment is presented in a new format using the data mining software to add

the inverse TNX rate to the ETF ratio.

Update. Bearish sentiment in ETFs saw a sharp spike last week, but prices

remain subdued due to high int rates and continued weakness in China (SSEC).

II. Dumb Money/Smart Money Indicators

This is a new hybrid option/ETF Dumb Money/Smart Money Indicator as a INT/LT

term (outlook 2-6 mns) bearish sentiment indicator. The use of ETFs

increases the duration (term).

Update. Bearish sentiment bounced off a strong Sell, but may also be

following the Jan-Feb 2021 path of a complex correction.

With the sister options Hedge Spread as a ST/INT indicator

(outlook 1-3 mns), bearish sentiment moved back to a strong Buy ST (grn) and

should help prices move higher and provide support from intraday weakness as

last weeks Thru-Fri declines.

A new composite SPX options indicator uses both the volume adj (1/B-A) and P/C

equivalent spread (A-B) to compensate for the discrepancy between the two.

This replaces the old SPX options indicator for the SPX ETFs + options below and the

INT/LT composite. No chart

For the SPX, I am switching to hybrid 2X ETFs plus SPX options. Taking a look at the

INT term composite (outlook 2 to 4 mns), bearish sentiment remains weak, but

may be bottoming as in May 2021.

For the NDX combining the hybrid ETF options plus NDX 3X ETF sentiment with the interest rate effect,

(outlook 2 to 4 mns) bearish sentiment shows similar extremes between ETF and

options as in late 2020 which resulted in a choppy market until options

sentiment rose. Note QQQ options are optimal, but are N/A and are included

in ETF options.

Bearish sentiment increased slightly with the Thur-Fri volatility, and

remains above neutral.

III. Options Open Interest

Using Thur closing OI, remember that further out time frames are more likely

to change over time, and that closing prices are more likely to be effected.

Delta hedging may occur as reinforcement, negative when put support is broken

or positive when call resistance is exceeded. This week I will look

out thru Sept 1. A text overlay is used for extreme OI to improve readability,

P/C is not changed. A new addition is added for OI $ amounts with breakeven pts (BE) where

call & put $ amounts cross.

With Fri close at SPX 4406, options OI for Mon is moderate with little OI bias

between 4375-4450, but deep ITM puts ($OI) may provide an upward bias toward

4425.

Wed has smaller OI where SPX outlook is about the same as Mon.

For Thur EOM strong OI has a positive bias to SPX 4450+.

For Fri Jobs report moderate OI has very strong put support at SPX 4400 and

below, and moderate support up to 4450, while call resistance starts at 4475 and

is strongest at 4500. A likely target may be around 4475.

IV. Technical / Other

The following uses barcharts.com as a source and discusses S&P futures (ES) as a third

venue of stock sentiment in addition to options and ETFs. The non-commercial/commercial

spread represents a LT bearish sentiment (dumb money/smart money) indicator. As explained in investopedia,

commercial investors (red) are institutions and are smart money, while non-commercials (green) are speculators such as

hedge funds and are dumb money. Here is the current barchart graph

for the S&P 500 (top) and trader positions (1st bot) with positives as net longs and negatives

as net shorts.

Bearish sentiment is represented by the spread and is positive if red > green

(Buy) and negative if green > red (Sell). ES sentiment is neutral at >

+.5 SD and now about the same as Sept 2020, YM (DJIA)

increased sharply to +.75 SD, Dow theory may keep DJIA up thru Sept-Oct, watch for Sell at -1 to -2 SD.

Click dropdown list to select from the following options:

Tech / Other History

2023

2022

Other Indicators

Conclusions. Sentiment is only slightly more bearish than last

week, except for the DJIA futures that may mean a return to relative strength

for the cyclicals vs techs. SPX options OI is indicating a possible

reverse of last week with a neutral Mon/Wed outlook and a Thru/Fri outlook for

gains to the mid 4450-4500 area. Fri with unemployment data shows very

large bearish sentiment and seems most likely to surprise to the upside.

Weekly Trade Alert. Prices may drift around early in the week, but

strength may return late in the week to about SPX 4475 by Fri close. Updates @mrktsignals.

The last few months, I indicated that stocks could continue tp rally with the

TNX below 4% and would face headwinds if rates rose over 4%, but last week and a

half the sustained breakout over 4% was more like a tornado. Rates rose

six days in a row thru Thur, reaching a new closing high of 4.3% compared to

4.25% Oct 2022 with the main culprit being Wed July's retail sales which caused

some to estimate Q3 GDP at 5%+ and the FOMC notes which were hawkish. The

SPX swooned Wed thru Fri AM dropping from 4450 to a Fri open at 4335.

The strength of the decline seemed to eliminate the traditional scenario

outline last week, so I am going to concentrate this week on the two more

bearish outcomes where much depends on the course of int rates (TNX). I

had been looking for a rounded bottom, or "cup and handle"

for the TNX where the "cup" sides are complete, but the "handle" implies a

retracement to about 3.8% before a breakout. If the handle forms there

could still be a retracement to the SPX 4550+ area in Sept which is also

consistent with the Thur EW outlook by Dr. Schure

(no J/S, reload). So Scenario 1 (50%) assumes that rates retrace and the SPX gap fills

at 4565. From there, the c-wave sees a-down of 272 pts (4607-4335) x 1.62

extension to 4125 for a 10% decline (see scenario 2 for rate dependency).

This would likely be an expanding wedge in price and time to EOY. Scenario

2 (50%) assumes that rates continue to rise where the lows will be about SPX 4125 if

rates remain below 5%, but over 5% a 15% decline to about SPX 3920 is likely by

EOY, this is also the 62% retrace of the entire rally from the Oct lows of 3490.

Sentiment is somewhat mixed with major distortion from new record volume in

SPX puts and calls (see DM section). The ST composite did reach a weak Buy

while the VIX call indicator is near a strong Buy. Other positive INT

indicators are the Hedge Spread that reached a ST strong Buy and the NDX indicator

that reached levels comparable to lows in 2020 and 2021. Bond sentiment

remains weak, but over the weak Sell. SPX options OI last week showed a BE

at/near 4300 which was surprisingly accurate and this week are a 4600 with large

EOM OI showing a BE of 4550. All together this seems to support a retracement

of 50%+.

I. Sentiment Indicators

The INT/LT Composite indicator (outlook 3 to 6+ months) has three separate

components. 1st is the SPX and ETF put-call indicators (40%), 2nd the SPX 2X ETF INT

ratio (30%), and 3rd a volatility indicator (30%) which combines the options

volatility spread of the ST SPX (VIX) to the ST VIX (VVIX) with the UVXY $ volume.

This week breaks SPX options into volume adj (1/B-A) and traditional spread (A-B).

Update Alt. In this case the wts for the SPX 2X ETF ratio (SDS/SSO) and SPX puts &

calls spread are adj to equal as in the DM/SM section for SPX ETFs. Bearish sentiment

shows a large drop mainly due to SPX options. The DM section shows a

drilldown of SPX puts & calls and record volume (0DTE) is likely distorting

sentiment.

Update Alt EMA. Bearish sentiment fell sharply.

The ST Composite as a ST (1-4 week) indicator includes the NYSE volume ratio

indicator (NYDNV/NYUPV & NYDNV/NYDEC) and the UVXY $ Vol/SPX Trend. Weights

are 80%/20%.

Update. Bearish sentiment reached the weak Buy level and means a ST rally is

likely soon.

Update EMA. Bearish sentiment is showing that ST EMAs are still similar to

May, so a strong advance is unlikely.

Also, looking at the ST VIX Call & SPXADP indicator, bearish sentiment is

near a strong Buy so lower VIX and higher SPX are likely for the next 2-4 weeks.

The ST/INT Composite indicator (outlook 1 to 3 months) is based on the Hedge Spread (48%)

and includes ST Composite (12%) and three options FOMO indicators using SPX (12%),

ETF (12%), and Equity (12%) calls compared to the NY ADV/DEC issues (inverted). FOMO

is shown when strong call volume is combined with strong NY ADV/DEC. See

Investment Diary

addition for full discussion.

Update EMA. Bearish sentiment has turned positive but remains below a weak

Buy, so a partial retrace for several weeks should start soon.

Bonds (TNX). Bearish sentiment shows a moderate uptick, so a

partial retrace is possible but not likely to last.

For the INT outlook with LT still negative, the gold miners (HUI) bearish

sentiment is presented in a new format using the data mining software to add

the inverse TNX rate to the ETF ratio.

Update. Bearish sentiment rose moderately. As discussed above if int

rates retrace, HUI may rally 10% back toward 235-40.

II. Dumb Money/Smart Money Indicators

This is a new hybrid option/ETF Dumb Money/Smart Money Indicator as a INT/LT

term (outlook 2-6 mns) bearish sentiment indicator. The use of ETFs

increases the duration (term).

Update. Bearish sentiment remains little changed.

With the sister options Hedge Spread as a ST/INT indicator

(outlook 1-3 mns), bearish sentiment saw a sharp move back to the strong Buy

level although LT EMAs are lagging. A strong retracement over the next

4-6 weeks is possible, but new highs are unlikely.

A new composite SPX options indicator uses both the volume adj (1/B-A) and P/C

equivalent spread (A-B) to compensate for the discrepancy between the two.

This replaces the old SPX options indicator for the SPX ETFs + options below and the

INT/LT composite. Here, I am showing the raw SMA puts& calls with ratio. The

extreme high volume (0DTE effect?) is usually bearish, while low P/C is bullish.

Large spikes in put buying is usually a ST bottom.

For the SPX, I am switching to hybrid 2X ETFs plus SPX options. Taking a look at the

INT term composite (outlook 2 to 4 mns), bearish sentiment fell sharply

mainly due to the extreme SPX optn volume.

For the NDX combining the hybrid ETF options plus NDX 3X ETF sentiment with the interest rate effect,

(outlook 2 to 4 mns) bearish sentiment shows similar extremes between ETF and

options as in late 2020 which resulted in a choppy market until options

sentiment rose. Note QQQ options are optimal, but are N/A and are included

in ETF options.

Bearish sentiment rose sharply over neutral, pulled upward by ETF options and

is at a level similar to Mar 2021 and could see a strong retrace of the current

decline.

III. Options Open Interest

Using Thur closing OI, remember that further out time frames are more likely

to change over time, and that closing prices are more likely to be effected.

Delta hedging may occur as reinforcement, negative when put support is broken

or positive when call resistance is exceeded. This week I will look

out thru Aug 25 & EOM. A text overlay is used for extreme OI to improve readability,

P/C is not changed. Also, this week includes a look at the GDX & TLTfor Sept exp.

A new addition is added for OI $ amounts with breakeven pts (BE) where

call & put $ amounts cross.

With Fri close at SPX 4370, options OI for Mon is moderate with strong put

support at 4375.but a gap below until 4300. Negative news could push

lower, but above 4375, 4400 is likely.

Wed has moderate OI where SPX with large put OI at 4460 and 4475 similar to

last week, but are now deep ITM. Aug flash PMIs are out early,

but likely to pull prices up over 4400 toward 4450.

For Fri stronger OI are likely to pull prices up toward the 4400-4450 level. .

For Thur EOM SPX has very large OI and a BE at 4550 and a move to 4450-4500 by

EOM looks likely.

Using the GDX as a gold miner proxy closing at 27.5, prices should push higher

toward 30-31.

Currently the TLT is 93.8 with the TNX at 4.25%, and should recover back toward

the 100+ level.

IV. Technical / Other

The following uses barcharts.com as a source and discusses S&P futures (ES) as a third

venue of stock sentiment in addition to options and ETFs. The non-commercial/commercial

spread represents a LT bearish sentiment (dumb money/smart money) indicator. As explained in investopedia,

commercial investors (red) are institutions and are smart money, while non-commercials (green) are speculators such as

hedge funds and are dumb money. Here is the current barchart graph

for the S&P 500 (top) and trader positions (1st bot) with positives as net longs and negatives

as net shorts.

Bearish sentiment is represented by the spread and is positive if red > green

(Buy) and negative if green > red (Sell). ES sentiment continues to

fall, now at +.5 SD, YM (DJIA)

is at neutral at 0 SD, Dow theory may keep DJIA up thru Sept-Oct, watch for Sell at -1 to -2 SD.

Click dropdown list to select from the following options:

Tech / Other History

2023

2022

Other Indicators

Conclusions. Last weeks economic news all but killed any hopes an

econimic slowdown any time soon and lower rates from the Fed. On the plus

side stronger growth usuually means stronger earnings hence the ebb and flow

pushing stocks lower as rates rise then higher when rates stabilize.

Hopefully, the lows will be seen in earnings in Oct-Nov as well as a good

portion of the high rates surprise, setting the stock market up for a positive

2024. As outlined above, the course of the stock market thru EOY will

likely include a 10-15% decline depending on int rates (TNX). Sentiment is

not that favorable for bonds which increases uncertainty. Aug 24-25 is

Jackson Hole where global CB leaders discuss outlook. Everyone has been

expecting China to come out with a big stimulus package, but this would likely

weaken the yuan. China may be concerned that if they support a gold-backed

currency, a weaker yuan means cheaper exchange prices for gold. No

stimulus from China may help lower int rates.

Weekly Trade Alert. A modest turnaround is expected next week for

the SPX to 4400-50 and possibly 4450-500 thru EOM. Updates @mrktsignals.

Last week was overall somewhat weaker than expected, but mostly within the

target range of SPX 4450-4550. The early bounce to SPX 4500+ (4518) only

lasted a day as weak data from China Tue set a negative tone to the market and

took prices back to the 4470s. Weakness lasted thru Wed with the expected

CPI rally lasting only about an hour, but did hit the target zone of SPX

4520-40 (4527). A disastrous 30 yr T-Bond auction Thur sent the LT bond

int rates back to test the prior weeks highs and reversed the SPX 55 pt gain to

a 15 pt loss by EOD. Higher PPI data Fri pressured TNX rates on Fri,

causing an SPX 15 pt loss for the week. On a positive note the SPX did bounce

off its 50 SMA and filled a gap at 4445-50. The question is will the gap at

SPX 4550-65 be filled before a larger down leg? The bad news is that bond

sentiment (TBT/TLT) is little changed and I am getting the same feeling I had in

mid-2021 right before TNX rates rose from 1% to 3%.

Today I want to look at three possible outcomes for the next 3-6 mns.

The first (prob 40%) is the contrarian view based on what I see sentiment wise.

I do think the will be a fill of the gap at SPX 4550-65, but sentiment is

currently too weak and a consolidation is likely to last thru Aug (range

4440-4500) similar to Apr-May. Then Sept with triple witch, FOMC and EOQ

the gap is filled. The high risk period is mid-Oct to mid-Dec when

inflation pressure and rising rates accelerate and EPS continues to disappoint,

pushing the SPX toward the 4100 area (top of A).

Second is the crash scenario (30%) for me the reason is rates continue to rise

due to higher inflation and new Treasury sales, pressuring Techs with the TNX

rising to 5-5.5% by EOY and the NDX filling a large gap around 13.5K and the SPX

down about 15%. Avi has a similar view, probably supported by an expected

banking crisis. In Avi's case

the SPX rises to 4550-65 for Aug optn exp, then down to 3800 by mid-Dec.

The third case which I call the traditional view (30%) is a decline into

Sept-Oct to about SPX 4300 then a rally into EOY to 4700-4800. Here we have

EW's Dr Schure (no J/S,reload)

and TA's ExecSpec.

Bond market sentiment is my biggest concern. An interesting article in

ZH

discussed some interesting divergences between futures (TN) and options (TLT)

which agreed with the extreme retail bullishness shown in the TBT/TLT sentiment

indicator. Otherwise sentiment is improving for the SPX/NDX but does not

indicate a strong turnaround for optn exp week. Due to the possible

influence of the Dow Theory a look at DJIA futures (YM) is included in the

Tech/Other section. The easiest way to view in COT is to edit url

replacing ES with YM and return. An additional link is added to Other

links for Marketwatch news releases (note Wed).

I. Sentiment Indicators

The INT/LT Composite indicator (outlook 3 to 6+ months) has three separate

components. 1st is the SPX and ETF put-call indicators (40%), 2nd the SPX 2X ETF INT

ratio (30%), and 3rd a volatility indicator (30%) which combines the options

volatility spread of the ST SPX (VIX) to the ST VIX (VVIX) with the UVXY $ volume.

This week breaks SPX options into volume adj (1/B-A) and traditional spread

(A-B).

Update Alt. In this case the wts for the SPX 2X ETF ratio (SDS/SSO) and SPX puts &

calls spread are adj to equal as in the DM/SM section for SPX ETFs. Bearish sentiment

declined slightly mainly due to SPX options.

Update Alt EMA. Bearish sentiment remains near the Sell level.

The ST Composite as a ST (1-4 week) indicator includes the NYSE volume ratio

indicator (NYDNV/NYUPV & NYDNV/NYDEC) and the UVXY $ Vol/SPX Trend. Weights

are 80%/20%.

Update. Bearish sentiment has barely touched the weak Buy level.

Update EMA. Bearish sentiment ST EMAs are just above neutral and suggest

more consolidation similar to Apr-May.

The ST/INT Composite indicator (outlook 1 to 3 months) is based on the Hedge Spread (48%)

and includes ST Composite (12%) and three options FOMO indicators using SPX (12%),

ETF (12%), and Equity (12%) calls compared to the NY ADV/DEC issues (inverted). FOMO

is shown when strong call volume is combined with strong NY ADV/DEC. See

Investment Diary

addition for full discussion.

Update EMA. Bearish sentiment continues to rise now above the weak Sell but

still below neutral, the level that supported most rallies in late 2020-21.

Bonds (TNX). Bearish sentiment remains near the Sell level and

is the most worrisome for stocks, esp NDX. Rates may continue to rise

for the next 3-6 mns.

For the INT outlook with LT still negative, the gold miners (HUI) bearish

sentiment is presented in a new format using the data mining software to add

the inverse TNX rate to the ETF ratio.

Update. Bearish sentiment fell sharply and seems to continue to follow the

mid-2018 analog. Probably the uptick in inflation excites the PM bulls,

but the negative interest rate effect should not be ignored. If inflation

and TNX rates continue to rise thru EOY, Fed will likely begin increasing ST

rates killing PMs.

II. Dumb Money/Smart Money Indicators

This is a new hybrid option/ETF Dumb Money/Smart Money Indicator as a INT/LT

term (outlook 2-6 mns) bearish sentiment indicator. The use of ETFs

increases the duration (term).

Update. Bearish sentiment is little changed.

With the sister options Hedge Spread as a ST/INT indicator

(outlook 1-3 mns), bearish sentiment rose sharply above the neutral level and

may increase enough to support a 2-3% rally in a week or two.

A new composite SPX options indicator uses both the volume adj (1/B-A) and P/C

equivalent spread (A-B) to compensate for the discrepancy between the two.

This replaces the old SPX options indicator for the SPX ETFs + options below and the

INT/LT composite. No chart.

For the SPX, I am switching to hybrid 2X ETFs plus SPX options. Taking a look at the

INT term composite (outlook 2 to 4 mns), bearish sentiment fell slightly due

to options extremes (0DTE effect?), while EFT sentiment is neutral.

For the NDX combining the hybrid ETF options plus NDX 3X ETF sentiment with the interest rate effect,

(outlook 2 to 4 mns) bearish sentiment shows similar extremes between ETF and

options as in late 2020 which resulted in a choppy market until options

sentiment rose. Note QQQ options are optimal, but are N/A and are included

in ETF options.

Bearish sentiment rose to the weak Sell level on the back of ETF option

sentiment while NDX ETF sentiment is little changed.

III. Options Open Interest

Using Thur closing OI, remember that further out time frames are more likely

to change over time, and that closing prices are more likely to be effected.

Delta hedging may occur as reinforcement, negative when put support is broken

or positive when call resistance is exceeded. This week I will look

out thru Aug 18. A text overlay is used for extreme OI to improve readability,

P/C is not changed. Also, this week includes a look at the GDX for Dec exp.

A new addition is added for OI $ amounts with breakeven pts (BE) where

call & put $ amounts cross.

With Fri close at SPX 4464, options OI for Mon is moderate and shows some

support for a rally to 4500, but there is little support until 4425.

Wed has somewhat smaller OI where SPX has very strong support at 4455 and 4470.

News (see Tech/Other Links) includes housing ind prod, and FOMC notes.

For Fri AM strong SPX OI levels with deep ITM calls skewing $ amounts, most

likely target 4450-4500..

For Fri PM moderate SPX OI levels with deep ITM calls skewing $ amounts, most

likely target 4450-4525..

IV. Technical / Other

The following uses barcharts.com as a source and discusses S&P futures (ES) as a third

venue of stock sentiment in addition to options and ETFs. The non-commercial/commercial

spread represents a LT bearish sentiment (dumb money/smart money) indicator. As explained in investopedia,

commercial investors (red) are institutions and are smart money, while non-commercials (green) are speculators such as

hedge funds and are dumb money. Here is the current barchart graph

for the S&P 500 (top) and trader positions (1st bot) with positives as net longs and negatives

as net shorts.

Bearish sentiment is represented by the spread and is positive if red > green

(Buy) and negative if green > red (Sell). ES sentiment is neutral,

but lower for the week at

< +1 SD, YM (DJIA)

is neutral at -0.1 SD, Dow theory may keep DJIA up thru Sept-Oct, watch for Sell at -1 to -2 SD.

Click dropdown list to select from the following options:

Tech / Other History

2023

2022

Other Indicators

Conclusions. Bearish sentiment for stocks is rising, but does

not indicate a strong rally next week. .Stocks, esp techs, will continued to be

pressured if rates continue to rise. Athough the SPX found support at its

50 SMA, NDX did not, and may indicate a problem. The DJIA continues to be

the stalwart and seems to bounce strongly every time 35k is tested. If the

DJIA remains strong,losses should be limited, but below the 34.7k level

problems may occur.

Weekly Trade Alert. Not expecting much action next week with the

SPX remaining in the 4440-4500 range unless bonds break down with TNX above

4.25-4.33%. Fri may see a late bounce over SPX 4500 if rates remain calm. Updates @mrktsignals.