Last week's outlook was for a rally into the EOY with possible ST tax loss selling driving the NDX and SPX lower first to 5800 and 2350, respectively. The NDX missed by 100 pts, while the Christmas Eve massacre drove the SPX to a close of 2351, and Tue gap up retest saw 2347 before a 120 pt romp upward into the close.

Last Dec, here and here, I was looking for a strong start in Jan 2018 to send a "false signal" via the January effect with weakness to follow similar to 1970-71. Jan 2019, I expect a similar, but opposite, "false signal" with a weak beginning but stronger prices for most of the year. In the forecast for 2019, I look at the biggest hurdles for higher prices for 2019 including China trade, Fed rate hikes and the Mueller report. Also discussed are three analogs including the 1970s, the 1998 LTCM crisis and the 2010 midterm period using sentiment measures $SKEW and $NYUPV/$NYDNV. So far the 1998 crisis, followed by a strong bull market to the 2000 top, seems the closest to the current market period with a closer look in the Technical Indicator section.

I. Sentiment Indicators

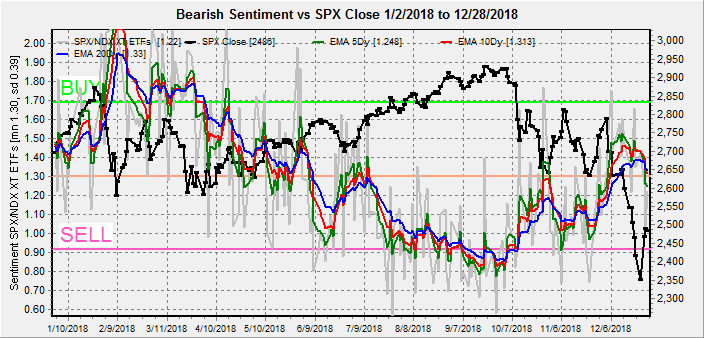

The overall Indicator Scoreboard (INT term, outlook two to four months) bearish sentiment has topped out slightly higher than the Mar-Apr retest and is consistent with an SPX 400+ pt rally.

The INT view of the Short Term Indicator (VXX+VXXB $ volume and Smart Beta P/C, outlook two to four months) bearish sentiment has reached the levels of the Feb lows, in a reverse pattern to the Feb-Apr period, but also consistent with an SPX 400+ pt rally.

Bond sentiment (TNX) continued to decline thru the week, matching the lowest levels of the year. Combined with the SPX/TNX ETF sentiment (2nd chart), the indication is that once money starts flowing back into stocks as happened last Apr, the rise in int rates will be stronger than Apr-Oct.

For the INT outlook with LT still negative, the gold miners (HUI) bearish sentiment is also nearing the levels seen in July before the meltdown from HUI 170 to 140. Suggesting that resolution of the China trade crisis could see sharp reversals for both bonds and gold stocks

II. Dumb Money/Smart Money Indicators

The Risk Aversion/Risk Preference Indicator (SPX 2x ETF sentiment/NDX ETF sentiment, outlook 2 to 4 wks/mns) as a INT indicator has dropped back to neutral showing that SPX and NDX should have similar performance.

The option-based Dumb Money/Smart Money Indicator as INT term (outlook 2 to 4 weeks/mns) moved from a strong SELL early Dec to a BUY, slightly stronger that the Mar-Apr retest and then moved back to neutral about where the Apr rally began.

The INT term SPX Long Term/Short Term ETFs (outlook two to four weeks/mns) bearish sentiment remains the most conservatively positioned indicator as the rise has been due to dumb money selling, but still no smart money buying. Rallies are likely to remain tepid until smart money buying picks up.

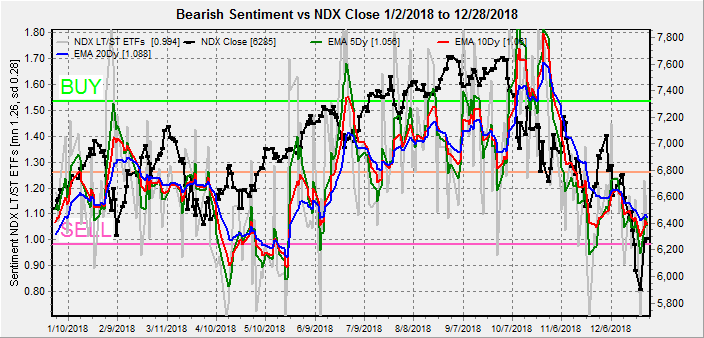

Long term neutral, the INT term NDX Long Term/Short Term ETF Indicator (outlook two to four weeks/mns) as the long cycle seems to follow prices, the short cycle has moved back to the long cycle trend.

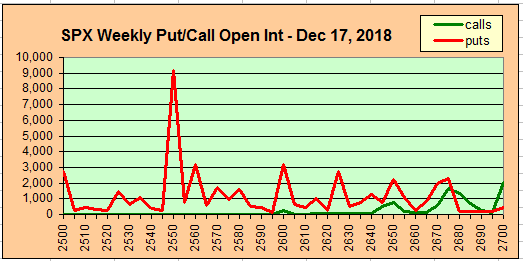

III. Options Open Interest

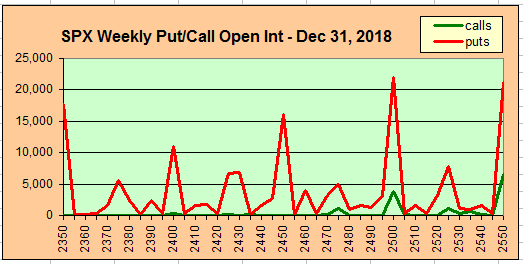

Using Thurs close, remember that further out time frames are more likely to change over time. M/F dominance by puts indicates inflection pts. This week I will look out thru Jan 4.

Mon with Fri close at SPX 2486. Below SPX 2500 there is a fluid range between 2450 and 2500 and strong support at 2400. Large open int, probably range bound.

Wed shows the strongest call resistance seen in a while at SPX 2525 as everyone seems to expect an up day. Fluid range between 2415 and 2490. Light open int overall.

Fri, jobs report, has large open int with SPX 2500 a major inflection pt. With all puts, its hard to draw any better conclusions. Over 2500 could show attraction to 2580.

IV. Technical / Other

Looking at the analog for the 1998 LTCM crisis that lasted six weeks compared to the current Oct-Dec decline that lasted twelve weeks it seems logical to apply a 2x timeline. After the lows on Sept 1, the SPX rallied for four weeks in a well define bear flag with about 6% rallies followed by 4% pullbacks in seven waves up. Today that would be about 4 up legs of 150+ pts with 100+ pt pullbacks, pointing to about SPX 2650-70 late Feb. Obviously analogs never work perfectly, but a pullback next week to 2400+ on govt shutdown fears followed by a strong rally over a compromise by next weekend would fit.

Conclusions. INT sentiment shows that the SPX is at/near a major bottom similar to Mar/Apr, but the SPX ETF Indicator is only at neutral so no strong rally is expected soon. The 1998 analog indicates a possible two month sawtooth rally to retrace 50% of the decline from SPX 2941 to about 2650 by late Feb. Mar is likely to see a return to volatility and a retest of the lows with the FOMC and China trade talks in focus. The Mueler report is expected out in Feb and may mark a ST top.

Weekly Trade Alert. The 1998 analog indicates a drop next week to the SPX 2400-20 area with a following rally of about 150 pts that could start Fri if a govt shutdown solution or other news is expected next weekend. Updates @mrktsignals.

Investment Diary, Indicator Primer, update 2018.03.28 Dumb Money/Smart Money Indicators

Article Index 2018 by Topic

Article Index 2017 by Topic

Article Index 2016 by Topic

Long term forecasts

© 2018 SentimentSignals.blogspot.com

{kind=link}

{kind=link}