This week's Tech/Other shows a followup of the Rydex Bear/Bull ETF Ratio, now in between the Jan and Sept 2018 lows, and the Crash Indicator which shows a less bearish view.

I. Sentiment Indicators

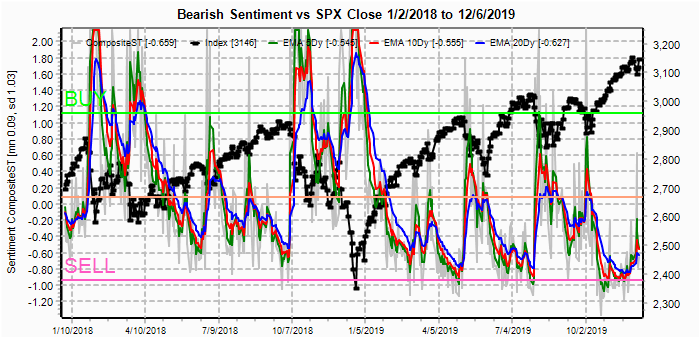

The overall Indicator Scoreboard (INT term, outlook two to four months) bearish sentiment has moved to the lowest level of the last two years (actually as far back as I could go, 2011). We should be approaching a significant top.

The INT view of the Short Term Indicator (VXX $ volume and Smart Beta P/C [ETF Puts/Equity Calls], outlook two to four months) bearish sentiment has also moved to the lowest level of the last two years.

Bonds (TNX). Interest rates were again turned down just below the 2.0% level, but the pattern of rising bottoms still supports higher rates, while sentiment remains extremely low.

For the INT outlook with LT still negative, the gold miners (HUI) came to life last week as the gold bugs are as resilient as Trump supporters, presumably due to talks of reflation after a China trade settlement, while bearish sentiment also remains extremely low.

II. Dumb Money/Smart Money Indicators

The option-based Dumb Money/Smart Money Indicator as short/INT term (outlook 2 to 4 mns/weeks) compared to other sentiment measures, options traders are still somewhat cautious and that may keep the rally going for a few weeks.

And the sister options Hedge Ratio sentiment is at levels comparable to other pullbacks, including the Oct 2018 10% decline, but we do not see crash levels similar to Jan or Dec 2018..

The INT term SPX Long Term (2x/DM) ETFs (outlook two to four weeks) bearish sentiment has now turned back down and may be tracing out a longer topping period as in Aug-Oct 2018.

The INT term NDX Long Term (2x/DM) ETFs (outlook two to four weeks) bearish sentiment has also turned back down.

Finally,a look at the 3X ETF ratio (TZA/TNA) for the RUT that has been outperforming lately and looks like it may make a double top around 1750, possibly due to hopes of a turnaround from China trade troubles.

III. Options Open Interest

Using Thur closing OI, remember that further out time frames are more likely to change over time, and that closing prices are more likely to be effected. This week I will look out thru Jan 3 with Mon/Tue/Fri where Tue is EOM. Also, This week includes a look at the GDX for Jan.

With Fri close at SPX 3240 after an early move up to 3248, Mon is somewhat similar to the last two weeks where there is little call resistance to higher prices up to 3270. However, Fri late futures are showing weakness, so a move to 3225 is possible.

Tue, EOM, is decidedly more negative with large open int showing the potential for a move down to the SPX "straddle" at 3200 (last week I incorrectly called this a strangle which uses diff strikes).

For Fri (no jobs reports until Jan 10), there is moderate to large OI with call resistance down to 3190 and no current put support until SPX 3175. Probably the best bet to hit 3200 or lower for the week.

Using the GDX (now 28.9) as a gold miner proxy. Where Dec opt exp showed a range of 26-28 as likely (which held until last week after opt exp), Jan exp shows a somewhat higher range with very large call resistance at 30 and little net put support until 25. Likely range 26-29.

IV. Technical / Other

A quick update of the Rydex Bear/Bull ETF Ratio shows a sharp spike lower last week below the 3.5% level, in between the Jan and Sept 2018 levels. An INT top should be near.

The Crash Indicator seems to have bottomed in the area prior to the Aug 2019 pullback of SPX 200 pts, but below that of the initial Oct 2018 down leg of 10%. This is consistent with a 7-10% pullback that may just be the initial leg of a larger decline as seen in Oct-Dec 2018.

Conclusions. Last week's strong seasonal bias was able to power thru SPX OI call resistance to higher levels, but the most likely scenario still seems to be a 1-3% pullback (w4 from TJ) before a more important top around mid Jan (opt exp, trade agreement, State of Union). The nature of the decline will likely become clearer after sentiment updates when normal trading returns. VIX call buying remains stubbornly low, but it also did not spike before the "mini flash crash", then again can anyone predict Trump's Tweet storms (much like CA earthquakes).

Weekly Trade Alert. Small pullback possible to SPX ~3200, then higher to mid Jan for INT top. Updates @mrktsignals.

Investment Diary, Indicator Primer, update 2019.04.27 Stock Buybacks, update 2018.03.28 Dumb Money/Smart Money Indicators

Article Index 2019 by Topic

Article Index 2018 by Topic

Article Index 2017 by Topic

Article Index 2016 by Topic

Long term forecasts

© 2019 SentimentSignals.blogspot.com