I. Sentiment Indicators

There was not a lot of change last week, so this will be brief. The overall Indicator Scoreboard retreated to a more bearish position as the SPX moved sideways.

The Short Term Indicator (VXX $ volume and Smart Beta P/C) has not reached the SELL level last seen before the mid-May decline, so today I am going to focus on the components. The VXX $ volume has dropped to the SELL level, but this alone has not been sufficient for much of a decline since the election.

The Smart Beta P/C continues to be the key for the Short Term Indicator as continued ETF hedging keeps this indicator from reaching the SELL level.

Before moving on, I want to take a look at one sector which may the culprit and that is the NDX/QQQ sentiment measure using the SQQQ/TQQQ ratio. As you can see this reached the BUY level and appears to have plenty of room for prices to move higher.

Sentiment for bonds (TNX) is consolidating at lower levels as interest rates have regained about half the loss since the election, but continues to face strong headwinds from higher short term rates and QE unwinding as well as higher inflation prospects from the Republican agenda.

Sentiment for gold stocks (HUI) with ST EMAs moved to slightly less bearish as prices seem to be coiling for a breakout one way or another.

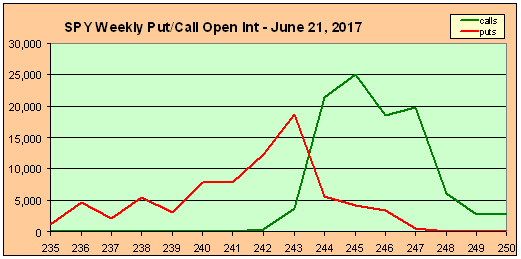

II. Options Open Interest

This week I am going to take a quick look at Friday's options, then look ahead for the next quarter by options expirations. For June 30, the likely range is 242 to 245 with the most likely 243.5. Note with SPY going ex-div SPX 2440/1 equals SPY 243.5.

For the monthlies in July, the range is much wider from SPY 240 to 247, so is probably the best chance for a move to 246-7.

For August, we have a setup almost identical to the QQQs in May where the most likely level is SPY 244 with identical puts and calls, but a move lower could quickly start delta hedging, pushing the SPY down to the 235 level. (So potential for mini crash.)

September is even more interesting with a bi-modal setup. This seems to reflect the outcome for a vote on the Trump tax cuts, pass then SPY goes to 250, don't pass the SPY goes to 230. Most likely is 240, but small number indicates low probability, and since puts (support) are slightly larger than calls (resistance), probability of up move seems more likely.

One last look at GDX shows a lower likely range of 20-23, but a move over 23 may result in delta hedging upwards to 24 then a sharp whipsaw as we saw in the NDX.

III. Technical Indicators

For some time I have been interested in volume indicators and earlier this year I noticed that the TRIN (which compares the number and volume of advancing and declining issues) pointed to strength while other indicators did not. So when I finally got some free time, last week I showed a volume based (lower supporting volume means higher risk) High Risk Indicator $NYAD:$NYUD, now revised to a 20 day SMA and cutoff of 5.0 that gives about a one month warning before a top. Then last week I came up with a Capitulation Indicator $NYDNV:$NYDEC, where high volume on declining issues points to a bottom. Interestingly both of these are at critical levels, but the Capitulation Indicator seems to be shorter term, so the predicted result would be higher prices first then a sizable decline.

The third volume indicator I found just playing around with LT SMAs and I am calling it the BUY/HOLD/SELL/Crash Indicator, $NYUPV:$NYDNV. Results varied greatly before 2013, but since then the 200 day SMA indicates SELL (not short) when the level drops to 1.5. seen Dec 2015 and last week, BUY when 2.0 is reached and HOLD to SELL. The 100 day SMA seems to work as a Crash Indicator when the value drops below 1.5 for a period of time; this occurred three times since 2013, Sept-Oct 2014, July 2015, and May-June 2017. So no guarantee what will happen this time, but the last half of 2014 is starting to look more likely.

Conclusions. Not much has changed since last week, except the day to day comparisons to 2014 seemed to fail, but similar results may still prevail. Technical indicators show higher prices short term are likely, but there is increased risk longer term. Sentiment agrees. Options open interest point to SPY 247 as a possible high between now and July 21, with the possibility of a decline into Aug 18 to SPY 235. September seems to be an interesting month depending on the outlook for the Trump tax cut program.

Weekly Trade Alert. I am going to preface my comment with a chart. The last three months seem to be a series of bull and bear flags. The latest, an upward sloping bear flag looks to need one more high that should be in the SPX 2460s next week or 2470s the week after. A breakdown would probably test the 50 day SMA. Result, Short on test of upper TL, target 50 day SMA.

Updates @mrktsignals.

Article Index 2017 by Topic

Article Index 2016 by Topic

© 2017 SentimentSignals.blogspot.com