Looking at the market's performance last week the minor pullback at the EOM is looking more like 1987, where a small pullback at the end of June was followed by higher highs in July, another small pullback then a melt up in Aug, than 2015, where the rally off a 38% retracement was followed by a volatile period leading to a retest before the distribution rally into May. Sentiment is also pointing in this direction and is highlighted in the Tech/Other section, where a followup of the data mining into the P/C ratios looks at the Smart Beta P/C (ETF puts/Equity calls) and shows why a melt up is consistent with other recent tops.

This week, I am converting to the new graphics update, but the only apparent differences are a slightly lighter background and tighter spacing of the legends. Everything worked OK except for HUI and BKX charts, so the HUI was done with the old software.

I. Sentiment Indicators

The overall Indicator Scoreboard (INT term, outlook two to four months) bearish sentiment continues to fall, but at a slowing rate, indicating that a multi month topping period as in 2015 or Jul-Oct 2018, or a sharp advance as in Jan 2018 or Mar-Apr 2019 is likely before a top is in.

The INT view of the Short Term Indicator (VXX+VXXB $ volume and Smart Beta P/C [ETF Puts/Equity Calls], outlook two to four months/weeks) bearish sentiment is nearing recent extremes, but it is interesting to note that the pattern since late 2017 is more extremes in low bearish sentiment before bigger declines. Does this indicate a megaphone pattern?

Bonds (TNX). Interest rates. We saw almost a year of high bearish sentiment from late 2017, so I guess the drop in rates should not be unexpected, but risks for bond holders abound as a China trade settlement could reverse the current economic slowdown, while impending food shortages from the mid west could dramatically increase inflation in food and gas (ethanol).

For the INT outlook with LT still negative, the gold miners (HUI) bearish sentiment has now fallen to extremes that marked tops/near tops since mid 2017. I missed this one, as the second spike in bearish sentiment in May produced a much stronger reaction than the one in Sep 2018.

II. Dumb Money/Smart Money Indicators

For this week and possibly for the next several months, I am going to replace the DM/SM ETF indicators with other indicators.

The option-based Dumb Money/Smart Money Indicator as short/INT term (outlook 2 to 4 mns/weeks) has shown a sharp drop that is more similar to Dec 2017 than to the rallies into the gradual topping leading into the Oct 2018 and Apr 2019 tops..

And the sister options Hedge Ratio sentiment is following a similar pattern and again may be implying a Dec 2017 type setup.

The INT term SPX Long Term (2x/DM) ETFs (outlook two to four wks/mns) bearish sentiment is falling more slowly and indicates that ETF investors are slow to embrace this rally, so we are unlikely near an important top.

The INT term NDX Long Term (2x/DM) ETFs (outlook two to four wks/mns) bearish sentiment is even less enthusiastic than the SPX ETFs. One possible outcome here is that the gov't investigations into monopolistic behavior absolves the big techs (so they can compete with Huawei) causing a buy spike later this summer.

III. Options Open Interest

Using Wed close, remember that further out time frames are more likely to change over time, and that closing prices are more likely to be effected. This week I will look out thru Apr 30. Also, This week includes a look at the TLT thru Jun.

Fri close at SPX 2942 leapt over the 2925 resistance with leaked news of China trade progess as Trump gave Huawei access to US tech to restart trade talks. For the week M/W/F are similar with moderate open int, all showing strong call resistance at 2950 so its difficult to say how much progress will be made during the week.

Wed, about the same. A strong move over 2950 could go to 3000.

For Fri, if over 2950, 3000 is possible, but more likely a close below 2950.

Using the GDX as a gold miner proxy, now at 25.5. For Jul exp, if GDX makes it over 26 there is little resistance above. There is little put support, so a reversal below24 seems likely. Progress in trade talks may dampen the demand for gold/stocks.

IV. Technical / Other

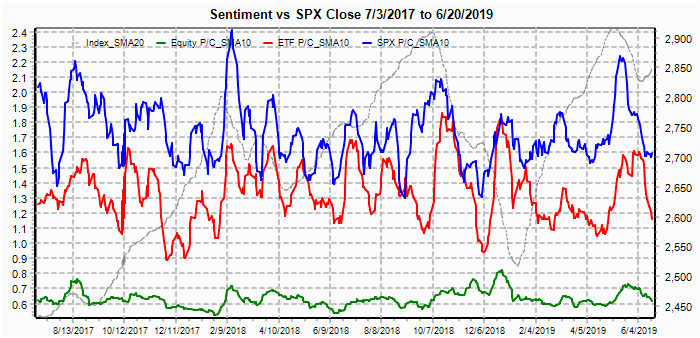

Last week, I showed a preview of the charting interface I built to datamine the indicators I have developed, mainly to see how they work and if the can be improved, but also to understand why they son't work sometimes such as the DM/SM ETF indicators. During the week I added the individual put/call categories and want to use that as a followup of last week's ratio comparison which showed that the ETF P/C seemed to be the best at identifying market tops.

More specifically, looking at the puts and calls separately the ETF put levels were more important, as are equity calls and together they make up the Smart Beta P/C. Individually they are shown back to Jul 2017. Each of the last three corrections were identified by spikes in equity calls (grn) and a collapse in ETF puts (red) although the timing has varied by a few weeks. For the Jan 2018 top. ETF puts bottomed in mid Dec 2017, while equity calls peaked at +2 SD in late Jan. For the Oct 2018 peak, equity calls peaked over +2 SD at the Sep highs, while ETF puts bottomed at the Sep high. For the Apr 2019 high, puts and calls both reached their extremes at the Apr high although equity calls only made it to +1.5 SD. Currently ETF puts are near the lows of Dec 2017, but the equity calls are far from any of the previous tops for SPX, near the Nov-Dec 2017 levels. This seems to imply that a melt up equivalent to Jan 2018 (+200 SPX pts) may be required to reach the same sentiment levels.

The following chart shows an overlay with the Smart Beta P/C (blue) that shows that more time (Jan 2018 top) or more extreme lows (Oct 2018, Apr 2019) is likely before a top.

Finally for comparison to the EMA model, where the 10 day EMA is about the same as the 10 day SMA/Std Var.

Conclusions. An imminent collapse seems unlikely as sentiment has not reached the levels seen at major tops since 2017, but the question as to whether this evolves as a lengthy distribution top or a Jan 2018 type melt up is unclear, and I'm about 50/50 either way. I have considered for several months now that one way out for Trump with the China trade situation is to offer a contingent plan to China where a 1 year trial period is used to see if enough progress is made for things like IP rights and other security issues. This would allow the economy to recover before the election, and he could get tough again right before or after the election, if re-elected. A sticky point is China's insistence of suspension of all tariffs before any agreement.

The Tech/Other section looks into the Smart Beta P/C components that show a sharp pickup in equity call buying is likely before a top is reached in the SPX. Possible developments that could lead to this result are a China trade settlement, Fed rate cuts starting in July, and/or clearing of the giant techs of monopoly charges.

If the SPX continues to follow the 1987 analog mentioned above, we should see the SPX Approach the 3,000 area by July opt exp on the 21st, a pullback to 2950, then a 200 pt run up in Aug. With the FOMC scheduled for Jul 30-1, this would fit in with a rate cut at that time.

Weekly Trade Alert. Trumps caving on Huawei's access to US tech has probaby started the SPX move to 3000. The alternation principle comparing the INT tops of Jan and Oct 2018 suggests that this top will be a melt up. Options open int suggest little progress this week, but a rally toward SPX for the Jul 21 opt exp seems likely. Updates @mrktsignals.

Investment Diary, Indicator Primer, update 2019.04.27 Stock Buybacks, update 2018.03.28 Dumb Money/Smart Money Indicators

Article Index 2019 by Topic

Article Index 2018 by Topic

Article Index 2017 by Topic

Article Index 2016 by Topic

Long term forecasts

© 2019 SentimentSignals.blogspot.com