Part I.

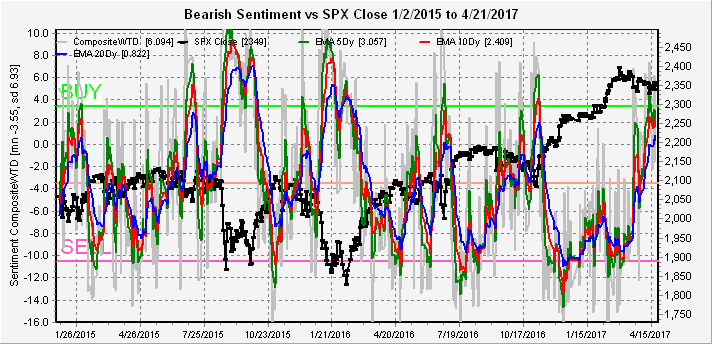

There is only a minor change in the overall Indicator Scoreboard as high intra day volatility kept the bears salivating and is why I expect any pullback to be bought. A gap down Monday to the SPX 2320-30 level is possible, but would present the same setup expected last week.

The Short Term Indicator (VXX $ volume and Smart Beta P/C) has pulled back closer to the mean, so it's unlikely that last weeks SPX 30 pt rally is duplicated. My new upside target is only about SPX 2370.

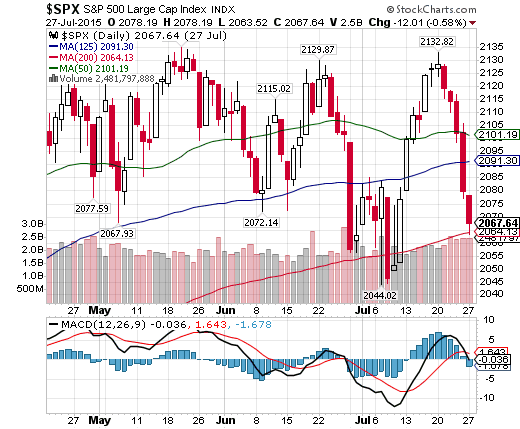

One of the largest changes in sentiment last week was in bonds (TNX). The last several weeks, I pointed out that rising bearish sentiment was likely to lead to lower rates, and last weeks drop to 2.2% sent the bears running for cover. Any further drop in rates is likely to setup a SELL, so stabilization or increase in rates is likely, and long term pressure is still up.

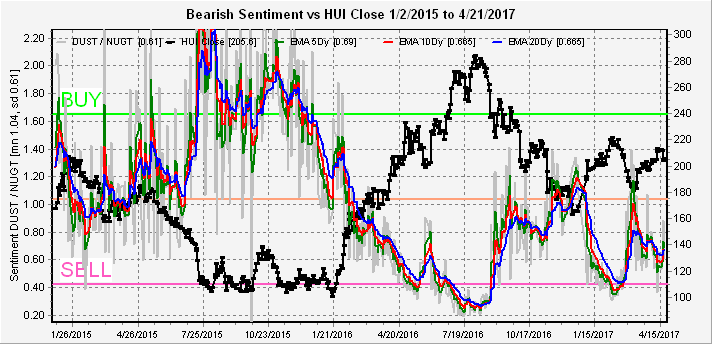

Gold stocks (HUI) seem to have stabilized in a trading range, but with bearish sentiment so low downside surprises are likely.

Part II. Risk Measures

Several weeks ago in March, here, I pointed that the high SKEW readings have generally led to large price moves, up or down, and combined with the overall Indicator Scoreboard indicated a down move was likely. We now have another spike in the SKEW, but the Indicator Scoreboard is now pointing upward. The overall pattern is similar to the Nov-Dec 2016 period.

Earlier in the year, I noted that low VIX P/Cs were common prior to sharp market declines as in June and Dec 2015, as well as Oct of 2016. But the low readings in Feb 2017 saw no declines, and I noticed that this may be due to the low TRIN. We again saw near record lows in the VIX P/C last week as Wed saw VIX calls equal to half of all CBOE daily call volume.

The past several weeks, I have been following the TRIN (net advances/net volume, rising as volume declines), noting that rising TRIN indicated rising risk with a spike higher two weeks ago duplicating the Dec 2015 levels.

Trying to combine the effects of the TRIN and VIX P/C, I added the inverse TRIN and the VIX P/C to create a High Risk Composite. It may sound a little weird, but since Jan 2015, I identified seven SELLs and the first six ALL produced declines of 3% or greater in the SPX in the following six to eight weeks, including the 10%+ declines of Aug 2015 and Jan 2016. Multiple signals over a short period were counted as one. The sixth signal was at the March top, and the seventh signal occurred last week. BUYs don't seem to be significant. There also seems to be an average lag of about two weeks before the bulk of the decline.

Conclusion. More volatility. One potential price pattern that seems to fit the current sentiment patterns is the May-July 2015 topping pattern. Here we saw a six week decline of 3% from the May top, followed by a three week rally (now, SPX 2370-80 by May 2017), then an even sharper decline of about 4% (now, debt ceiling panic), concluded by a final rally to test ATH (now, EW fifth wave).

Weekly Trade Alert. I would be inclined to go LONG a retest of the SPX 2320s, but prefer to play it safe to see if there is a rally into May 3 FOMC as many are starting to hope for slow down in rate hikes. This fits the High Risk Composite time frame for a SHORT if S/T Indicator drops to SELL. Updates @mrktsignals.

No comments:

Post a Comment