2015.03.. Long term forecast. Are high stock prices reasonable in a low growth economy?

2015.11 #1 First use of composites to combine indicators as standardized variables.

2015.11 #2 Sell signal generated with composite at -1 SD, expecting 10+% decline in SPX.

2015.11 #3 Closer look at the VXX $ volume indicates max risk in Dec-Jan.

2015.11 #4 Possible rally into Thanksgiving, revising the CPC for VIX component.

2015.11 #5 Using short/long ETFs to develop synthetic put/call ratios.

2015.11 #6 Use of short/long ETFs for HUI indicate 50-60% rally likely for gold stocks.

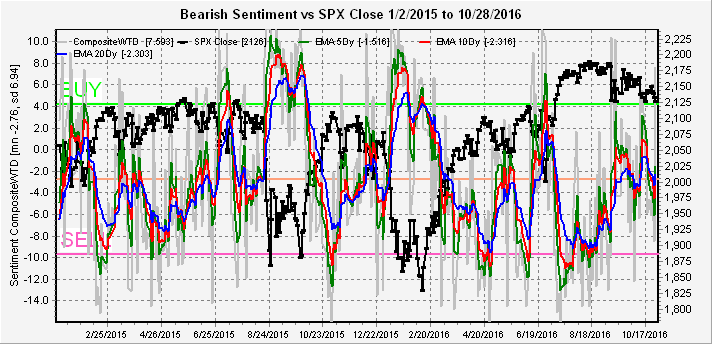

2015.12 #1 A look at composites and several ETF indicators.

2016.01 #1 Sentiment update.

2016.01 #2 Bearishh sentiment rising, a look at TBT/TLT for bond sentiment.

2016.01 #3 Bearishh sentiment nearing extreme but could go higher, ETFs for RUT and NDX,.

2016.01 #4 Use of sentiment models in bear markets, what to look for after Mar-Apr rally.

2016.02 #1 Rising bearishness and a spike in VIX P/C indicate washout ahead followed by sizable rally.

2016.02 #2 Some indicators showing strong buy while others are neutral.

2016.02 #3 Drop in bearish sentiment for HUI but too early to be negative. Students Trifecta composite.

2016.03 #1 Using Students Trifecta more rally likely but expecting summer pullback.

2016.03 #2 First attempt at Indicator Scoreboard.

2016.03 #3 Students Trifecta composite indicates a short term top is near.

2016.03 #4 Extremes of some individual indicators may support continued strength.

2016.04 #1 Indicators pointing to a pullback, but not a final top. Bonds and gold trending sideways.

2016.04 #2 Too early to be short, a look at intermediate and long term volatility measures.

2016.04 #3 A look at composites and ETFs, no immediate sell signals.

2016.04 #4 Using stastical correlations with indicators and expected returns (back tested).

2016.05 #1 Setting up an overall Indicator Scoreboard using correlations as weightings.

2016.05 #2 Expecting a short term rally then lower lows.

2016.05 #3 Nearing a bottom.

2016.05 #4 Setting up for a rally.

2016.05 #5 Topping pattern may extend four or five months.

2016.06 #1 Rangebound markets, backtesting Indicator Scoreboard for 2013-14.

2016.06 #2 Looking for expansion of trading range, strong bounce after panic low below SPX 2085.

2016.06 #3 Strong rally likely after BREXIT vote due to volatility blowout.

2016.06 #4 Sentiment unclear as strong rally lowers bearishness.

2016.07 #1 Positive bias for now with higher risk for August.

2016.07 #2 Unclear for SPX, but HUI low bearish extremes pointing to significant top.

2016.07 #3 Some but not all indicators at low extremes, expecting top by EOY. Use of Short Term Indicator.

2016.07 #4 Review of various composites.

2016.07 #5 Short term top is likely.

2016.08 #1 Low bearish sentiment continues, but risk of significant decline unlikely until after election.

2016.08 #2 Similarities to first half of 2015, but short term volatility may increase.

2016.08 #3 Still locked in tight range.

2016.08 #4 Looking for brief decline before move to SPX 2200.

2016.09 #1 More consolidation.

2016.09 #2 Sharp decline before BREXIT, indicators neutral.

2016.09 #3 Spike in bearishness for SPX likely point to new ATH, recent complaceny in HUI means lower lows.

2016.09 #4 Topping process continues.

2016.10 #1 Short term indicator has a long way to go before a SELL.

2016.10 #2 Sentiment points to higher interest rates, lower gold stocks, but neutral for SPX.

2016.10 #3 Possible short term dip but double buy spike in ST Indicator points to strong rally.

2016.10 #4 Expecting strength before election, sharp decline then rally.

2016.10 #5 Concerns over Hillarys emails may push SPX down to 2100 before election.

2016.11 #1 Spike in bearish sentiment likely to lead to fast and furious rally post-election, still negative on gold.

2016.11 #2 Long term indicators pointing to 15-20% correction over next 12 months, but no immediate decline. Gold and bonds following sentiment patterns.

2016.11 #3 Am I the only bear? Indicator Scoreboard same as EOY 2015, but ST Indicator neutral.

2016.11 #4 Bearish sentiment continues to fall but no official SELL. Bond sentiment spikes, HUI sideways.

2016.12 #1 With sentiment so low Santa Claus rally may be over early this year.

2016.12 #2 Overall Indicator Scoreboard reaches SELL level, but STI still supportive of higher prices.

2016.12 #3 Fed rate hike crashes gold and sends rates soaring, but sentiment only yawns.

2016.12 #4 Short Term Indicator now at a SELL. A LT look at the BKX using FAZ/FAS etfs.

2016.12.. Long term forecast. What Happens When Growth Returns?