I. Sentiment Indicators

This week I am taking a long term look at the Indicator Scoreboard and Short Term Indicator back to the 2015 period. The overall Indicator Scoreboard (INT term, outlook two to four months) rose sharply nearing the BUY level. Comparing the flash crash of Aug 2015 to the Feb 2018 drop, the June 2018 sentiment lows (price highs) fell below the early Nov 2015 sentiment lows, but has now rallied strongly matching that of the Nov 2015 SPX selloff.

The INT view of the Short Term Indicator (VXX $ volume and Smart Beta P/C, outlook two to four months) also rallied sharply last week almost reaching the mid-Dec 2015 levels. In both cases, the 2015 analog would argue for a clearing rally to SPX 2770-80 to reset sentiment before a much larger decline is likely.

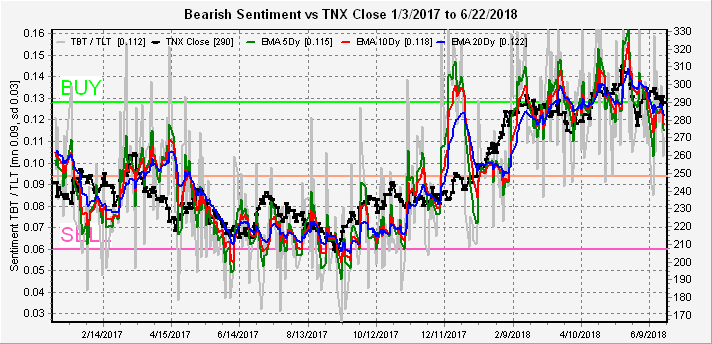

The high bearish bond sentiment (TNX) has continued to produce a consolidation in interest rates much as the low sentiment did for lower rates in mid to late 2017.

For the INT outlook with LT still negative, the gold miners (HUI) bearish sentiment fell sharply as prices rebounded Friday. Given the recent period of modestly high bearish sentiment, more upside is possible but not likely to be the beginning of a major uptrend.

II. Dumb Money/Smart Money Indicators

The Risk Aversion/Risk Preference Indicator (SPX 2x ETF sentiment/NDX ETF sentiment, outlook 2 to 4 days/hours) as a very ST indicator continues to languish in neutral territory, but well off the recent lows.

The option-based Dumb Money/Smart Money Indicator as short/INT term (outlook 2 to 4 days/weeks) has reversed sharply from the lowest level of the year two weeks ago to matching the late March SPX lows. The mid-Mar to mid-Apr chop is pretty much what I expect thru the July earnings season.

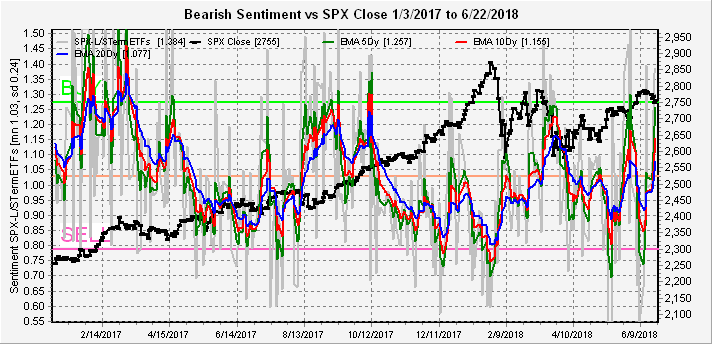

The INT term SPX Long Term/Short Term ETFs (outlook two to four weeks) rose very sharply due to strong selling in the 2x SDS/SSO sentiment while the 3x sentiment remained near neutral. This one is more difficult to interpret, but similar levels in Apr and Aug of 2017 saw choppy prices followed by rallies.

The INT term NDX Long Term/Short Term ETF Indicator (outlook two to four weeks) is now up to the July 2017 lows in the NDX.

III. Options Open Interest

Using the Thur closing data. SPX option open int worked well for last Mon/Wed showing little put support above SPX 2700, while Fri closed right at put support near 2720.

With Wed a holiday, options are for Mon/Tue which are very light, and Fri. For Mon, there is put support below SPX 2730 with large put position at 2760 that can act as a magnet if 2730 is exceeded. Could be a strong day.

For Tue, with extremely small option size and half trading day, the chart shows a "weak expected" SPX 2750 close and a potential range of 2690-2780.

Fri has large option contract size and since July 6 is the official start of the trade wars, some pullback might be expected. But options open int shows strong put support at SPX 2700 and 2725 with fairly strong resistance at 2750, so a likely range of 2725 to 2750 is expected.

Conclusions. Last week saw a 100 pt pullback similar to Nov 2015 with intra day volatility sending bearish sentiment soaring, but still much less than Aug 2017. Sentiment indicators are all over the place with short term bullish targets from the option-based DM/SM Indicator and SPX options open int to SPX 2750-60. The most likely INT outcome is a chop for most of July between lows of SPX 2675-2700 and 2750-60, followed by a breakout to the upside to reset bearish sentiment before a larger decline. It is likely that the SPX 50, 100 and 200 day SMAs converge before a large decline.

Weekly Trade Alert. None. Mon could see a small opening decline with SPX 2700 a possible inverse H&S target as well as 2716 to fill an opening gap, but a following move up over 2730 could reach 2750-60 by EOD. Updates @mrktsignals.

Investment Diary, Indicator Primer, update 2018.03.28 Dumb Money/Smart Money Indicators

Article Index 2018 by Topic

Article Index 2017 by Topic

Article Index 2016 by Topic

Long term forecasts

© 2018 SentimentSignals.blogspot.com