I. Sentiment Indicators

The overall Indicator Scoreboard remained very high but is now below the level of the 2015 flash crash prior to a retest.

The Short Term Indicator (VXX $ volume and Smart Beta P/C) has also fallen to levels below that prior to the 2015 flash crash retest.

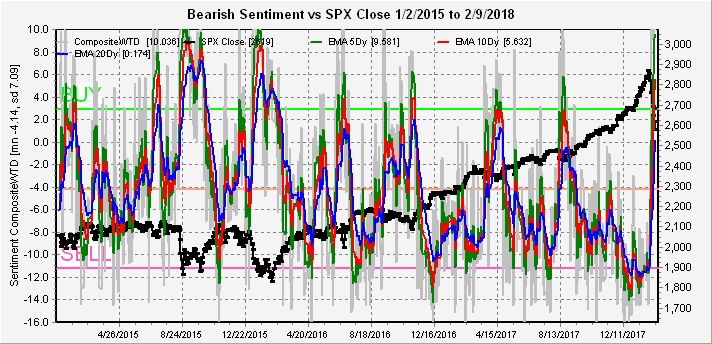

Looking at two of the equity ETFs, first the "buy and hold" SDS/SSO for the SPX, the level of fear indicated by the extreme bearishness resembles that after the Jan 2016 decline when many EW analysts were calling for a new bear market, but was instead followed by a 50% rise over the next two years.

Also, looking at the "revised" NDX SQQQ/TQQQ ETF ratio, bearish sentiment is literally off the chart as the readings maxed out at 1.45,1.25 and 1.05 (5,10,20 EMAs) on Feb 12 and still remain over 1.0. It is hard to say what this means for the NDX, but another 500 to 1,000 pts may be possible.

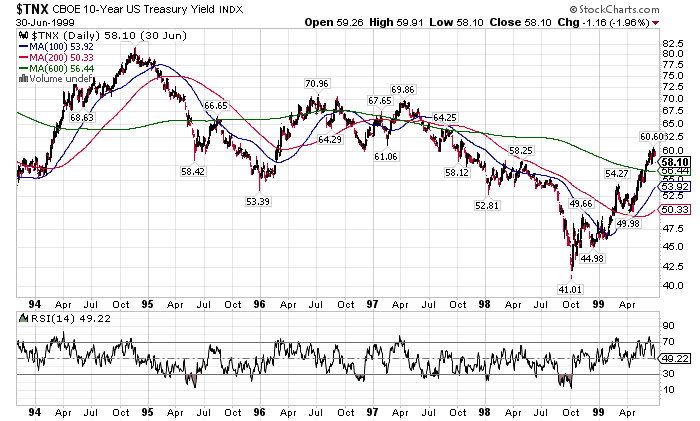

Bearish bond sentiment (TNX) is approaching the levels seen at the end of 2016 following a rise of 1.2%, but a similar rise this time would be to 3.3% so higher rates seem likely after the current consolidation period. More on what might cause higher rates in the technical indicator section.

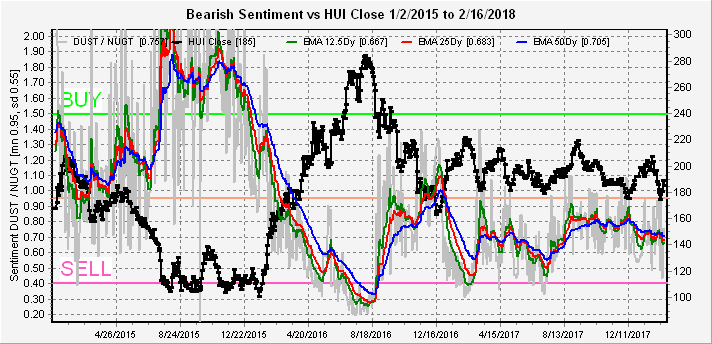

The gold miners (HUI) bearish sentiment continues to be a snooze fest, and prices are likely to drift lower.

II. Options Open Interest

SPY (close 274.7, SPX 2747) starts trading M/W/F options next week. Mon has only small positions but show delta hedging over 230 with a "most likely" of 272 on a drop below 230. For Wed, "most likely" is SPY 272-73, but only small resistance from 274 to 278, so a hold over 274 could push to 278 or higher while a drop below is like to move to 272-73.

For Fri, about all you can say is there is strong support at SPY 270 and below, while there is little resistance as far as the eye can see. As discussed in the TI section for the Aug-Sep 2015 fractal, this would be the ideal place for a "pop and drop" as high as the ATH at 285.

III. Technical Indicators

The recent bond consolidation/bearish sentiment picture makes the 1994 fractal less likely near term, but last weeks action is similar to Sep 2015 before the flash crash retest. Here we saw a consolidation mid-Sep below SPX 1960 (same as 2018 50 SMA 2730) before a 60 pt or 3% short covering rally on a breakout, which today would be about SPX 2800. The time frame between the two lows is 5 weeks which would be around the Mar 9 jobs data for 2018. Longer term, six months after the 2015 flash crash, we had the Jan 2016 decline that could correspond to June 2018 which is more likely to see the next run up in rates (TNX) given current bond sentiment.

A more bullish view by an EW analyst sees the Jan/Feb decline as a 4th wave correction, likely a triangle, before a 5th wave to SPX 3200. Sentiment using SDS/SSO and TQQQ/SQQQ does seem to support this view.

Finally a look at what seems to be the main driver of higher int rates (TNX) over the last few months, the US two year bond (red). The UST2Y is usually considered to be a measure of the expected Fed funds rate (FFR) plus 0.5% and the TNX (black) seems to be following it higher. Currently at 2.25% the UST2Y is reflecting a March FFR of 1.75% with 100% certainty, as June approaches, it will move to 2.5% if a rate hike is likely and carry the TNX over 3%.

Conclusions. Last week saw the early pullback and sharp rally back, but at higher levels than expected. The opening gap down was a signal that a top was going to be delayed and was warned of on Twitter. The most interesting fact was that on Wed when the DJIA was up strongly after the Fed minutes release, after the TNX jumped .05%, the DJIA fell over 300 pts; next on Fri when the TNX dropped .05%, the DJIA jumped back up over 300 pts. Its hard to believe, but sentiment, especially equity ETFs, now seem to be aligning for a 1999 mega blowout in the NDX with SPX in tow. However, this is also consistent with my favored long term forecast of a 1970-72 type bear market, where we saw a series of 10% corrections every few months (now rising rate fears as well as liquidity crises as in China, etc) with each correction followed by 70-80% retracements in the DJIA ([75% is 25,800], now due to high bearish sentiment). We could also see something like mid-2015 on a larger scale, where the SPX had several highs around 2130, while the NDX continued to make new highs.

Weekly Trade Alert. Next week may be a replay of last week if the SPY options open int is any indication. We may retest the SPX 50 SMA from above and it should be a buying oppty if bonds hold steady. Possible consolidation thru Wed with a late week explosion upward with a target of SPX 2800+. The Wed spike selloff may be a "false positive" making everyone complacent if it happens again, but if Sep 2015 repeats it will be the real deal with a decline probable to at least SPX mid 2600s thru Mar 09+. BUY at SPX 2720-30s, SELL at low 2800s. The most interesting question is what happens if Fri closes at a high over 2800, will it be like Jan 26 or will the next Mon be a "pop and drop"? Updates @mrktsignals.

Investment Diary, Indicator Primer, update 2018.02.23 ETF Sentiment Revision

Article Index 2018 by Topic

Article Index 2017 by Topic

Article Index 2016 by Topic

Long term forecasts

© 2018 SentimentSignals.blogspot.com