Two weeks ago I began warning that a large negative bias was present in the SPX Dec 20 options open int. At this point I should confess that I have been using $ OI base on 1 share/contract so that amounts are actually 100 times what was stated, and a note was added this week. The warning was that weakness similar to the Nov exp was expected, but in Nov there was a negative call bias of $350B whereas in Dec the bias was $1.6T or almost 5 times as much, so after the FOMC decision, which was widely expected, options dealers started selling futures creating a spiral of falling prices with stops triggering the last hour. The BE for the Fri AM was SPX 5900, but I had expected it to hold and instead prices fell to a low of 5830 before a strong reversal. Sentiment, however, is much the same as after a longer selloff over the month of Sep 2021 which was followed by a multi-month rally of about 10% (see Tech/Other) into the Jan 2022 top. This could mean an Apr-May top in 2025.

One thing that was glossed over by the media were the comments that Powell made with the FOMC decision about bitcoin ($BTCUSD). Essentially he said (no J/S) that the Fed was not authorized to hold crypto and indicated skepticism about holding speculative assets. Likely this means that Congress, Treasury and the Fed all need to agree on setting us a strategic reserve of bitcoin. Probably, a new more receptive Fed appointed by Trump in 2026 is needed. An interesting EW scenario by Dr. Shure discusses one way this could playout with a 50% correction in BTC into 2026 before a SC5 blowoff. In case this does work out I have decided to add an occasional options OI for IBIT the Blackrock BTC ETF starting this week.

ST sentiment is now at a strong Buy, but still faces the large call wall at SPX 6050 at Dec EOM.

I. Sentiment Indicators

The INT/LT Composite indicator (outlook 3 to 6+ months) has three separate components. Starting Aug 26, 2023 SPX options are removed due to extreme 0DTE volume distortions. New weights are ETF put-call indicator (30%), SPX 2X ETF INT ratio (40%), and 3rd a volatility indicator (30%) which combines the options volatility spread of the ST SPX (VIX) to the ST VIX (VVIX) with the UVXY $ volume.

Update Alt, INT view. Bearish sentiment remained in a narrow range.

Update. Bearish sentiment rose from a weak Buy to a strong Buy.

Update EMA. Bearish sentiment continued to rise but remained below neutral.

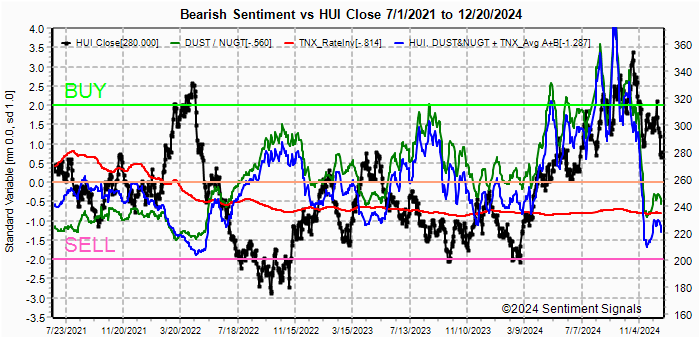

Update. Bearish sentiment remains below a weak Sell, where sentiment and prices trend look similar to mid-2022 and from a slightly higher level which could mean a lower target around HUI 200.

II. Dumb Money/Smart Money Indicators

This is a new hybrid option/ETF Dumb Money/Smart Money Indicator as a INT/LT term (outlook 2-6 mns) bearish sentiment indicator. The use of ETFs increases the duration (term).

Update. Bearish sentiment is little changed.

For the SPX, I am switching to hybrid 2X ETFs plus SPX options. Taking a look at the

INT term composite (outlook 2 to 4 mns), bearish sentiment remains near

neutral.

Bearish sentiment remains below a weak Sell with weak hedging.

Bearish sentiment for SPX is little changed.

III. Options Open Interest

Using Thur closing OI, remember that further out time frames are more likely to change over time, and that closing prices are more likely to be effected. Delta hedging may occur as reinforcement, negative when put support is broken or positive when call resistance is exceeded. This week I will look out thru Dec 31. A text overlay is used for extreme OI to improve readability, P/C is not changed. Also, this week includes a look at the GDX for Dec exp. A new addition is added for OI $ amounts with breakeven pts (BE) where call & put $ amounts cross. Note multiply OI$ by 100 for shares/contract.

With Fri close at SPX 5931, options OI for Mon is moderate with strong put support to the low 5900s should see 5900+ (Sat debt ceiling passed).

For Fri SPX OI is small, but prices could push toward BE at mid-6000s.

Currently the TLT is 88.3 with the TNX at 4.52%, have fallen thru strong put resistance at 90 and could fall toward 87 with BE at 93. ETF sentiment above is a negative.

Currently the IBIT is 54.8 with $BTCUSD at 96.9k, low P/C is one reason why BTC is weak with lower put support at 48-9

IV. Technical / Other

Several months ago, I tried to setup a more complex composite to mirror the earlier composites before I started the data mining project. As it turns out, it works pretty well as a ST/INT indicator although there a too many lines to read, but the EMAs are clearer.

Called the Technical Indicator Composite, the past several months have shown sentiment similar to mid-2021 with the current sentiment matching that of the Sept 2021 decline which was followed from a 10%+ rally from below SPX 4300 to 4800+ for the next four months to Jan 2022. From the 5830 low, a 10% rally is 6400+.

The following uses barcharts.com as a source and discusses S&P futures (ES) as a third venue of stock sentiment in addition to options and ETFs. The non-commercial/commercial spread represents a LT bearish sentiment (dumb money/smart money) indicator. As explained in investopedia, commercial investors (red) are institutions and are smart money, while non-commercials (green) are speculators such as hedge funds and are dumb money. Here is the current barchart graph for the S&P 500 (top) and trader positions (1st bot) with positives as net longs and negatives as net shorts. Bearish sentiment is represented by the spread and is positive if red > green (Buy) and negative if green > red (Sell). ES (SPX) sentiment remains a positive +0.25 SD, NQ (NDX) bearish sentiment remains a strong Sell at -2.25 SD, YM (DJIA) remains a weak Sell -1.0 SD.

Click dropdown list to select from the following options:

Tech / Other History2024

2023

2022

Other Indicators

Conclusions. Although ST sentiment is showing a strong Buy, the

INT/LT sentiment, including the hedge spread remain weak, so although I think

the markets may rally for several months, it is likely to remain fairly volatile.

Weekly Trade Alert. SPX options OI is indicating that a rally into

the low-mid 6000s is possible next week, starting with news of a budget

compromise, but a pullback is likely into EOM. Updates @mrktsignals.

Investment Diary,

Indicator Primer,

Tech/Other Refs,

update 2021.07.xx

Data Mining Indicators - Update, Summer 2021,

update 2020.02.07 Data Mining Indicators,

update 2019.04.27 Stock Buybacks,

update 2018.03.28 Dumb Money/Smart Money Indicators

Article Index 2019 by Topic, completed thru EOY 2020.02.04

Article Index 2018 by Topic

Article Index 2017 by Topic

Article Index 2016 by Topic

Long term forecasts

© 2024 SentimentSignals.blogspot.com